Image data:

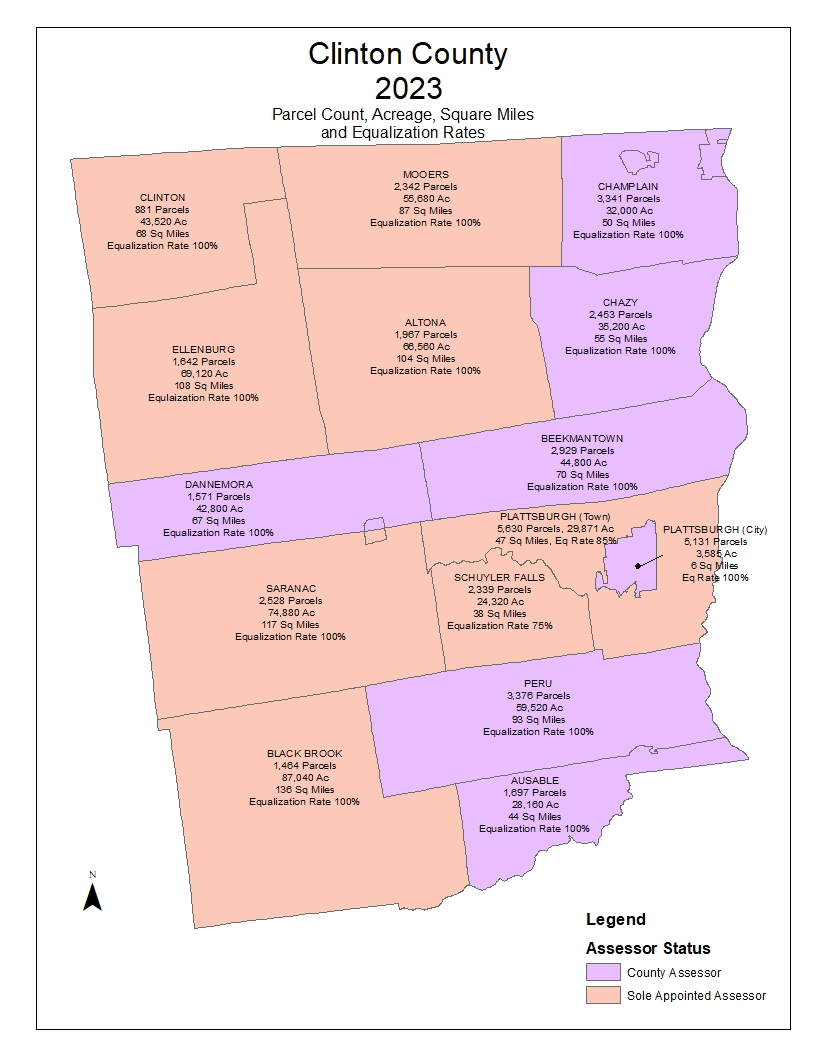

| SWIS | TOWN | EQUALIZATION RATE | # OF PARCELS | # OF ACRES | # OF SQ. MILES |

| 092000 | Altona | 100% | 1,970 | 66,560 | 104 |

| 092200 | Ausable | 100% | 1,697 | 28,160 | 44 |

| 092400 | Beekmantown | 100% | 2,930 | 44,800 | 70 |

| 092600 | Black Brook | 100% | 1,464 | 87,040 | 136 |

| 092800 | Champlain | 100% | 3,341 | 32,000 | 50 |

| 093000 | Chazy | 100% | 2,453 | 35,200 | 55 |

| 093200 | Clinton | 100% | 881 | 43,520 | 68 |

| 093400 | Dannemora | 100% | 1,572 | 42,800 | 67 |

| 093600 | Ellenburg | 100% | 1,642 | 69,120 | 108 |

| 093800 | Mooers | 100% | 2,342 | 55,680 | 87 |

| 094000 | Peru | 100% | 3,376 | 59,520 | 93 |

| 094200 | Plattsburgh (Town) | 85% | 5,630 | 29,871 | 47 |

| 094400 | Saranac | 100% | 2,528 | 74,880 | 117 |

| 094600 | Schuyler Falls | 75% | 2,339 | 24,320 | 38 |

| 091300 | City of Plattsburgh | 100% | 5,130 | 3,585 | 6 |

| TOTAL | 39,295 | 697,056 | 1,090 | ||

| As of 2023 Final Roll | |||||

| Altona John Brunell Phone 518-236-7035 ext 102 Fax 518-236-7621 |

Town Office PO Box 79 Altona, NY 12910 |

Office Hours: Cell Phone: (386) 279-1952 |

| Ausable Sean Masten Phone 518-834-9052 Option 8 Fax 518-834-9519 |

Town Office 111 Ausable Street Keeseville, NY 12944 |

Office Hours: Town Office: Tuesday 8:30am-3:30pm; Fridays Assessor out in municipality reachable by phone Government Center: Monday-Friday 8am-4pm 518-565-4760 assessor@townofausable.com |

| Beekmantown Trevor Finley Phone 518-563-4650 Option 5 Fax 518-563-0554 |

Town Office 571 Spellman Rd West Chazy, NY 12992 |

Office Hours: Town Office: Every Monday 8:30am-3:30pm; Tuesdays Assessor out in municipality reachable by phone Government Center: Monday-Friday 8am-4pm 518-565-4760 beekmantownassessor@gmail.com |

| Black Brook Leon Brousseau Phone 518-647-5411 Option 7 Fax 518-647-1294 12912 |

Town Office PO Box 715 Ausable Forks, NY 12912 |

Office Hours: Hours Vary or By Appointment townofblackbrookassessor@yahoo.com |

| Champlain Timothy Surpitski Phone 518-298-8160 Option 7 Fax 518-298-8896 |

Town Office 10729 Route 9, PO Box 3144 Champlain, NY 12919 |

Office Hours: Town Office: Every Thursday 8:30am-3:30pm; Mondays Assessor out in municipality reachable by phone Government Center: Monday-Friday 8am-4pm 518-565-4760 assessor@townofchamplain.com |

| Chazy Jeremiah Cross Phone 518-846-7544 Option 3 Fax 518-846-8981 |

Town of Chazy Assessor PO Box 219 Chazy, NY 12921 |

Office Hours: Town Office: Every Wednesday 8:30am-3:30pm, Thursdays Assessor out in municipality reachable by phone Government Center: Monday-Friday 8am-4pm 518-565-4760 chazyassessor@westelcom.com |

| Clinton Stewart Seguin Phone 518-569-0449 |

6199 Military Turnpike Ellenburg Depot, NY 12935 Town of Clinton 518-497-6133 |

Office Hours: By Appointment Only seguinmaple@gmail.com |

| Dannemora Trevor Finley Phone 518-492-7541 Option 5 Fax 518-492-7314 |

Town Office 78 Higby Road Ellenburg Depot, NY 12935 |

Office Hours: Town Office: Every Wednesday 8:30am-3:30pm; Thursdays Assessor out in municipality reachable by phone Government Center: Monday-Friday 8am-4pm 518-565-4760 assessor@townofdannemora.com |

| Ellenburg Stewart Seguin Phone 518-594-7708 Fax 518-594-7414 |

Ellenburg Municipal Building 16 St Edmunds Way Ellenburg Center, NY 12934 |

Office Hours: By Appointment Only assessor@townofellenburg.com |

| Mooers Larry Wolff Phone 518-236-7927 ext 107 Fax 518-236-4769 |

Town Office 2508 Route 11, PO Box 242 Mooers, NY 12958 |

Office Hours: Every Tuesday 9am-3:30pm mooersassessor@mooersny.com |

| Peru Jeremiah Cross Phone 518-643-2745 ext 104 Fax 518-643-0078 |

Town Office 3036 Main Street Peru, NY 12972 |

Office Hours: Town Office: Every Tuesday 8:30am-3:30pm; Mondays Assessor out in municipality reachable by phone Government Center: Monday-Friday 8am-4pm 518-565-4760 assessors@perutown.com |

| Plattsburgh, City of Timothy Surpitski Phone 518-565-4760 Fax 518-565-4773 |

Clinton County Real Property 137 Margaret Street, Suite 210 Plattsburgh, NY 12901 |

Office Hours: Monday-Friday 8am-4pm cityassessor@clintoncountygov.com |

| Plattsburgh, Town of Brian Dowling Phone 518-562-6820 Fax 518-563-8396 |

Town Office 151 Banker Rd Plattsburgh, NY 12901 |

Office Hours: Monday-Friday 8am-4pm briand@townofplattsburgh.org |

| Saranac Dave Galarneau Phone Office 518-293-6666 Option 6 Fax 518-293-7245 Home 518-647-8068 |

Town Office PO Box 147 Saranac, NY 12981 |

Office Hours: Every Wednesday 10:30am-4:30pm & Every 2nd and 4th Monday 5pm-7pm assessor@townofsaranac.com |

| Schuyler Falls Gary Drollette Phone 518-563-1129 Option 7 Fax 518-561-7845 |

Town Office 997 Mason St., PO Box 99 Morrisonville, NY 12962 |

Office Hours: Every Monday 8:30am- 3:30pm or By Appointment gary.drollette@schuylerfallsny.com |

Who is the Assessor?

What Training Does the Assessor Have To Take?

Assessors must obtain basic certification by New York State within three years of taking office*. This requires the successful completion of orientation, three assessment administration course components, and five appraisal components, including farm appraisal for certain agricultural communities. The New York State Office of Real Property Tax Services (ORPTS) prescribes the components.

*Assessors in Nassau County, Albany, Buffalo, Rochester, Syracuse, and Yonkers are not required to obtain basic certification.

Each year, appointed assessors must complete an average of 24 hours of continuing education. Both elected and appointed assessors may attain any of three advanced designations awarded by ORPTS: State Certified Assessor-Advanced, State Certified Assessor-Professional, and State Certified Assessor-National.

What Does an Assessor Do?

The assessor is obligated by New York State law to maintain assessments at a uniform percentage of market value each year. The assessor signs an oath to this effect when certifying the tentative assessment roll -- the document containing each property assessment. The physical description (or inventory) and value estimate of every parcel is required to be kept current. In order to maintain a uniform roll, each year your assessor will need to analyze all of the properties in the municipality to determine which assessments need to be changed.

Where assessments need to be changed, in some cases, your assessor will be able to increase or decrease the assessments of a neighborhood or group of properties by applying real estate market trends to those properties. This is possible only when the assessments to be changed are at a uniform level other than the municipality's stated level of assessment. In other cases, the assessor will need to conduct physical reinspections for reappraisals of properties. Every assessing unit should be keeping all assessments at a fair and uniform level every year.

The assessment roll shows assessments and appropriate exemptions. Every year the roll, with preliminary or tentative assessments, is made available for public inspection. After the Board of Assessment Review (BAR) has acted on assessment complaints and ordered any changes, the tentative assessment roll is made final.

What Kind of Property is Assessed?

All real property, commonly known as real estate, is assessed. Real property is defined as land and any permanent structures attached to it. Some examples of real property are houses, gas stations, office buildings, vacant land, motels, shopping centers, saleable natural resources (oil, gas, timber), farms, apartment buildings, factories, restaurants, and, in most instances, mobile homes.

How is Real Property Assessed?

Before assessing any parcel of property, the assessor estimates its market value. Market value is how much a property would sell for, in an open market, under normal conditions. To estimate market values, the assessor must be familiar with all aspects of the local real estate market.

A property's value can be estimated in three different ways. First, property is compared to others similar to it that have sold recently, using only sales where the buyer and seller both acted without undue pressure. This method is called the market approach and is normally used to value residential, vacant, and farm properties.

The second way is to calculate the cost, using today's labor and material prices, to replace the structure with a similar one. If the structure is not new, the assessor determines the depreciation since it was built. The resulting value is added to an estimate of the market value of the land. This method, called the cost approach, is used to value special purpose and utility properties.

The third way is to analyze how much income a property (like an apartment building, store, or factory) will produce if rented. Operating expenses, insurance, maintenance costs, financing terms, and how much money expected to be earned are considered. This method is called the income approach.

Properties in sub optimal uses generally may not be assessed at market value; they must be assessed at their current-use value.

Assessors with computers can estimate values more efficiently than by hand. Computer Assisted Mass Appraisal (CAMA) techniques are used to analyze sales and estimate values for many properties at once.

Once the assessor estimates the market value of a property, its assessment is calculated. New York State law provides that all property within a municipality be assessed at a uniform percent of market value. The level of assessment can be five percent, 20 percent, 50 percent, or any other fraction, up to 100 percent. Everyone pays his or her fair share of taxes as long as every property in a locality is assessed at the same percent of value.

For example, a house with a market value of $100,000 located in a town that assesses at 15 percent of value would have an assessment of $15,000. The assessment is multiplied by the tax rate for each taxing jurisdiction - city, town, village, school district, etc. - to determine the tax bills.

Does the Assessor have to be let into your home?

The New York State Assessors' Association pamphlet, “Understanding Assessments and Property Taxes,” states:

The Assessor has a right to go to your front door and seek admittance (possibly he or she will only want to inspect the exterior of the house) but must leave the premises if asked to do so.

If it is really inconvenient to allow an inspection at that time, tell your visitor just that and try to make an appointment for some other date. However, if you can spare the ten minutes or so that will usually be required, we urge that you allow it to proceed so that the information necessary for equitable assessment can be gathered.

The pamphlet cautions property owners not to allow anyone into their homes without proper identification, preferably I.D. cards with photographs signed by an authorized town or city official. "No identification — no entry!"

What Else Does an Assessor Do?

The assessor performs many other administrative functions, such as inspecting new construction and major improvements to existing structures. This ensures that the record of each property's physical inventory is current and that the appropriate improvements are assessed.

The assessor also approves and keeps track of property tax exemptions. Among the most common is the senior citizen, School Tax Relief (STAR), veterans, agricultural, and business exemptions.

The Real Property System is a computer software package (created and maintained by ORPTS) to assist assessment administration functions. It is available to assessors who have the necessary computer equipment, and allows them to electronically maintain the assessment roll and related records. Corrections to State form RP-5217 can also be sent to the State Board electronically. The Real Property System also includes computer-assisted mass appraisal programs for value estimation and assessment updates.

Legally, the assessor must be present at all public hearings of the Board of Assessment Review (BAR). The BAR may request the assessor to present evidence in support of tentative assessments being grieved by taxpayers. After meeting in private without the assessor, the BAR makes its decisions and orders any appropriate changes to the assessment roll before it becomes final. If assessment reductions are denied by the BAR, and property owners appeal to Small Claims Assessment Review, the assessor prepares evidence for those hearings.

The assessor reviews every transfer of real property for accuracy, including the basic information on the buyer, seller, and sale price. Assessment records are updated, and any unusual conditions affecting the transfer are also verified. Results are recorded on form RP-5217 at the real estate closing. The assessor makes corrections to this form.

ORPS requires assessors to file an annual report on assessment changes. ORPTS also "equalizes" property assessments to a common full (market) value in each municipality. More information on the ORPTS full value measurement program is available.

Where Can I Go With Questions?

The assessor is continually communicating with the public, answering questions, and dealing with concerns raised by taxpayers. Anyone can examine the assessment roll and property records at any time. However, between Taxable Status Day and the filing of the tentative roll (generally, March through May), it should be done by appointment.

It is up to individual property owners to monitor their own assessments. Taxpayers who feel they are not being fairly assessed should meet with their assessor before the tentative assessment roll is established. In an informal setting, the assessor can explain how the assessment was determined and the rationale behind it.

Assessors are interested only in fairly assessing property in their assessing unit. If your assessment is correct and your tax bill still seems too high, the assessor cannot change that. Complaints to the assessor must be about how property is assessed.

Taxpayers unhappy with growing property tax bills should not be concerned only with assessments. They should also examine the scope of budgets and expenditures of the taxing jurisdictions (counties, cities, towns, villages, school districts, etc.) and address those issues in appropriate and available public forums.

Informal meetings with assessors to resolve assessment questions about the next assessment roll can take place throughout the year. If, after speaking with your assessor, you still feel you are unfairly assessed, the booklet, “How to File For a Review of Your Assessment” describes how to prepare and file a complaint with the Board of Assessment Review for an assessment reduction, and indicates the time of year it can be done.